FD Laddering Strategy Explained

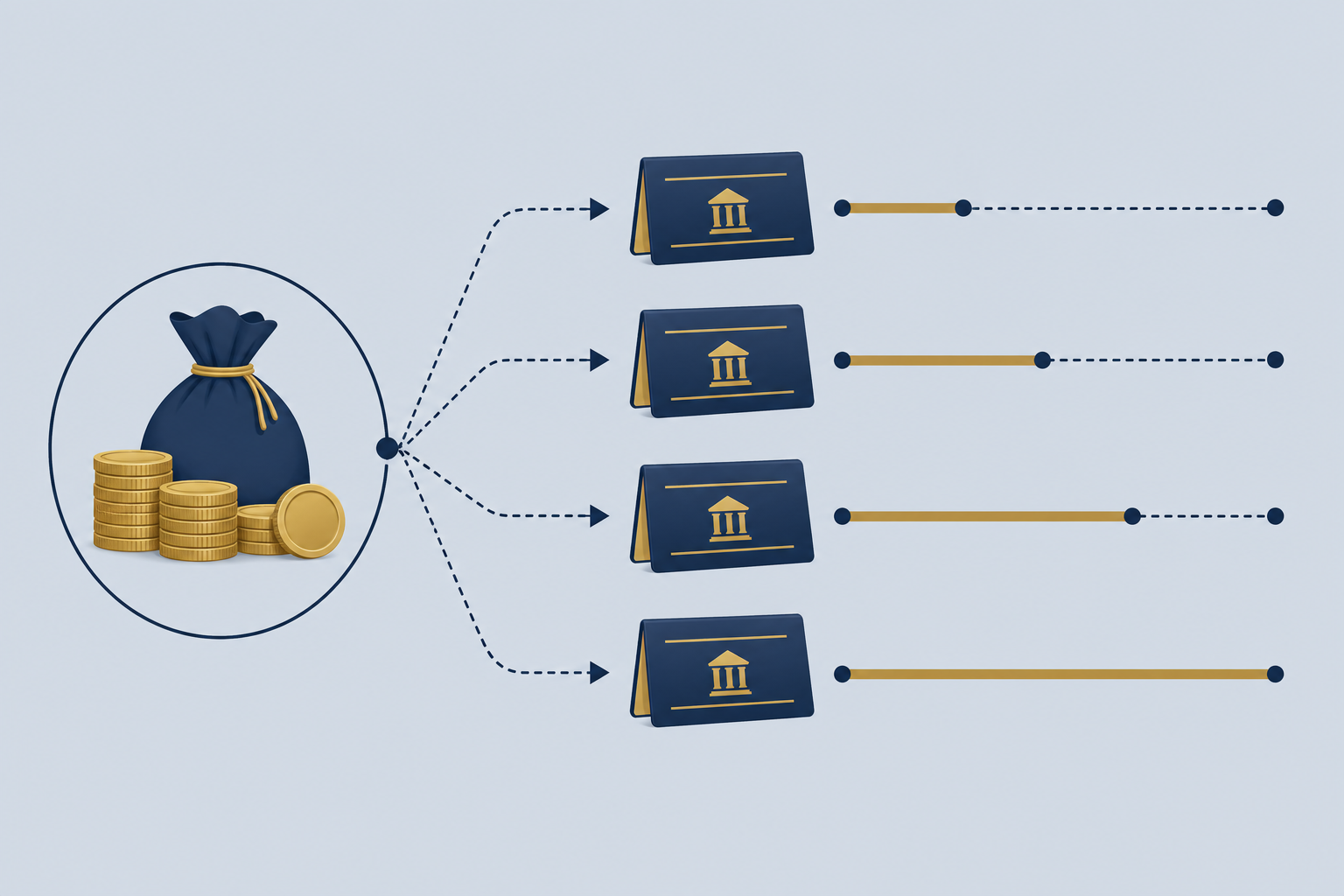

Want better FD flexibility without giving up returns? Then FD laddering can help. In short, you split one large deposit into smaller FDs with different tenures.

First, make sure you know the basics in What is Fixed Deposit?. Next, compare options in FD vs Savings Account. Finally, use our FD Calculator to test each ladder part.

On this page

What Is FD Laddering?

FD laddering is a simple deposit plan.

Instead of putting all money into one FD, you open a few FDs.

Moreover, each FD has a different tenure.

As a result, your money matures in steps, not all at once.

For example, you might open FDs for 1 year, 2 years, 3 years, 4 years, and 5 years. Then, every year, one FD comes due.

After that, you can use the money, or renew it for a longer tenure. Therefore, you keep both growth and access.

Why Does It Help?

Laddering helps in three clear ways.

Better cash access

First, you get money back at regular intervals. So, you do not wait years for every rupee.

Less rate risk

Next, rate changes hurt less. If rates rise later, you can renew a mature FD at the new rate.

Fewer early breaks

Also, you may avoid premature withdrawal penalties. That is because short FDs cover near-term needs.

Clear planning

Finally, goals become easier. You can match each FD to school fees, travel, or home repairs.

In contrast, one long FD can lock funds for a long time. Meanwhile, a short FD may earn less. Laddering sits in the middle.

To understand rate differences by tenure, read FD Interest Rates Explained.

How Does It Work?

Here is the basic idea.

You take one lump sum. Then you divide it into equal parts.

After that, you place each part in a different tenure.

Over time, the shortest FD matures first.

Then the next one matures. Then the next.

Meanwhile, the longer FDs keep compounding. For the difference between simple and compound interest, see Simple vs Compound Interest.

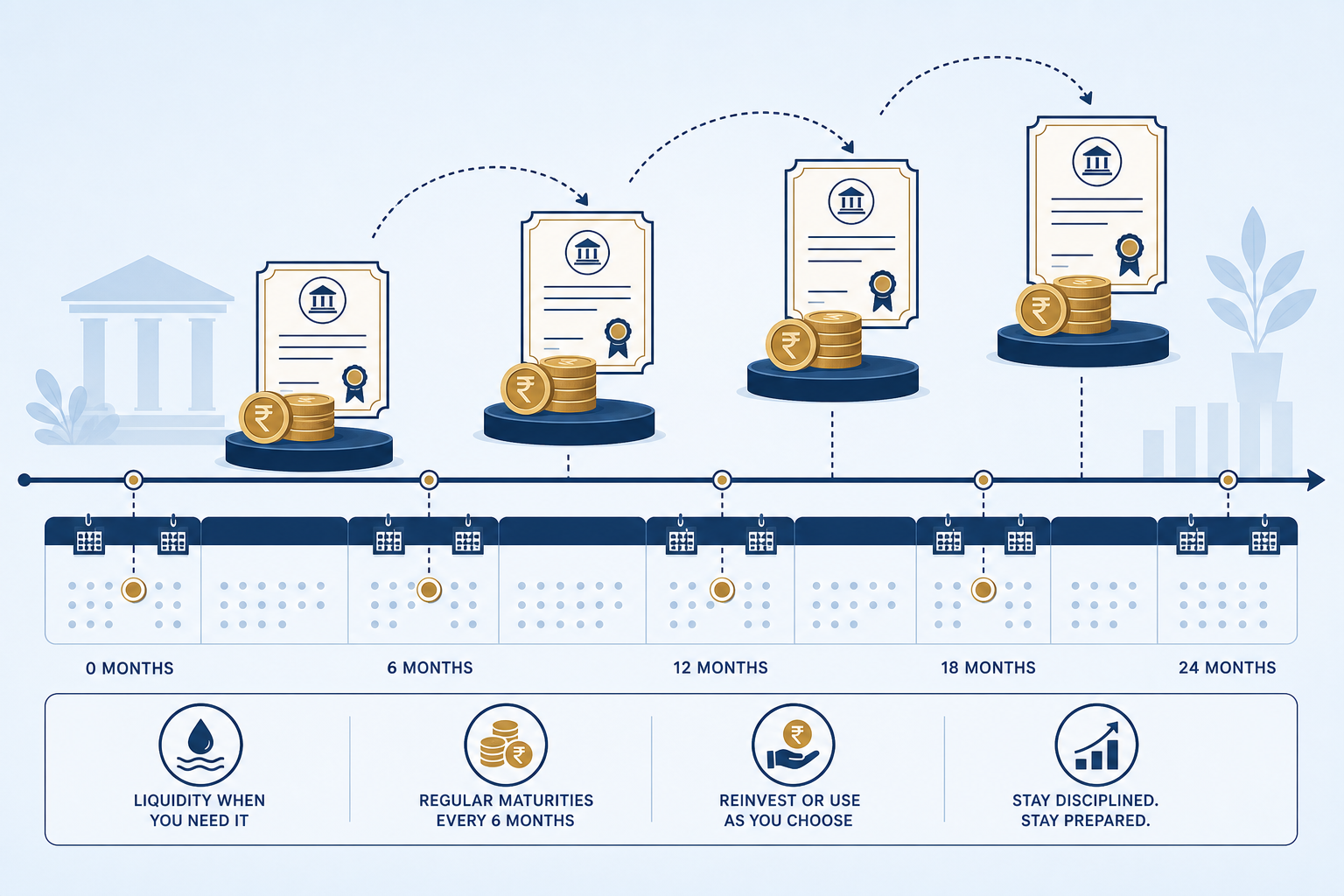

A Simple Example

Suppose you have ₹5,00,000 to invest.

Instead of one 5-year FD, you build a 5-step ladder.

| Ladder part | Amount | Tenure | What happens |

|---|---|---|---|

| FD 1 | ₹1,00,000 | 1 year | Matures first. You can use or renew it. |

| FD 2 | ₹1,00,000 | 2 years | Matures in year 2. |

| FD 3 | ₹1,00,000 | 3 years | Matures in year 3. |

| FD 4 | ₹1,00,000 | 4 years | Matures in year 4. |

| FD 5 | ₹1,00,000 | 5 years | Matures last and often earns a longer-tenure rate. |

After year 1, FD 1 comes back.

Then you can renew it for 5 years.

Later, when FD 2 matures, you renew that one for 5 years too.

As a result, your ladder slowly becomes a set of long-term FDs. However, you still get a maturity every year.

Tip: Run each ladder part in the FD Calculator before you book. Then compare bank tools like the HDFC FD Calculator, SBI FD Calculator, and Axis Bank FD Calculator.

Step-by-Step Guide

- Set your goal. First, decide why you need the money. Emergency buffer? Home repair? Child education?

- Keep some cash aside. Next, leave emergency money in a savings account. Do not lock every rupee.

- Choose the ladder size. Then pick 3, 4, or 5 FDs. Equal parts are easiest to track.

- Pick tenures. After that, space them out. Common choices are 1–2–3 years, or 1–2–3–4–5 years.

- Check rates. Meanwhile, compare current bank rates. Senior citizens often get a small extra rate.

- Calculate each part. Then estimate maturity with an FD calculator. Write down amount, rate, and maturity date.

- Book and track. Finally, open the FDs and save the maturity dates. When one matures, decide: spend, shift, or renew.

Smart Tips

- Start small if you are new. For example, begin with three FDs. Then grow the ladder later.

- Match tenure to needs. If you may need money in 12 months, keep one short FD.

- Renew with a plan. When an FD matures, renew it for the longest step in your ladder. This keeps yearly maturity going.

- Watch tax rules. Interest can attract TDS above bank limits. So, track interest across all FDs.

- Compare banks calmly. A slightly higher rate helps. But service, premature rules, and safety also matter.

For booking steps at one major bank, see Book a Fixed Deposit (HDFC).

Common Mistakes

Putting all money in long FDs

This can raise returns. However, it reduces flexibility. If plans change, early exit may cost a penalty.

Making too many tiny FDs

More FDs mean more tracking. Therefore, keep the ladder simple. Three to five parts is enough for most people.

Ignoring maturity dates

If you miss a maturity date, auto-renewal may lock money again. So, set reminders before each due date.

Skipping the calculator

Guessing returns is risky. Instead, estimate each part first. Then adjust amounts before you book.

Frequently Asked Questions

What is FD laddering in simple words?

FD laddering means splitting one big deposit into smaller FDs with different tenures, so money matures at different times.

Is FD laddering better than one long FD?

It depends on your needs. Laddering gives more flexibility and regular access to cash, while one long FD may be simpler to manage.

How many FDs should I open in a ladder?

Many people start with three to five FDs. Keep the count small enough that you can track each maturity date easily.

Can I use a calculator for FD laddering?

Yes. Run each ladder part separately in an FD calculator, then add the maturity amounts to see your total plan.

Does laddering reduce interest rates?

Not by itself. Each FD earns the rate for its own tenure. Some short FDs may earn less than a long FD, but you gain liquidity.