Simple vs Compound Interest in Fixed Deposit

Understanding how interest is calculated can make a big difference in your FD returns. This guide explains simple interest and compound interest in plain language, with formulas and practical examples.

If you are new to fixed deposits, start with What is Fixed Deposit?. You can also check how FD interest rates are decided before comparing calculation methods.

On this page

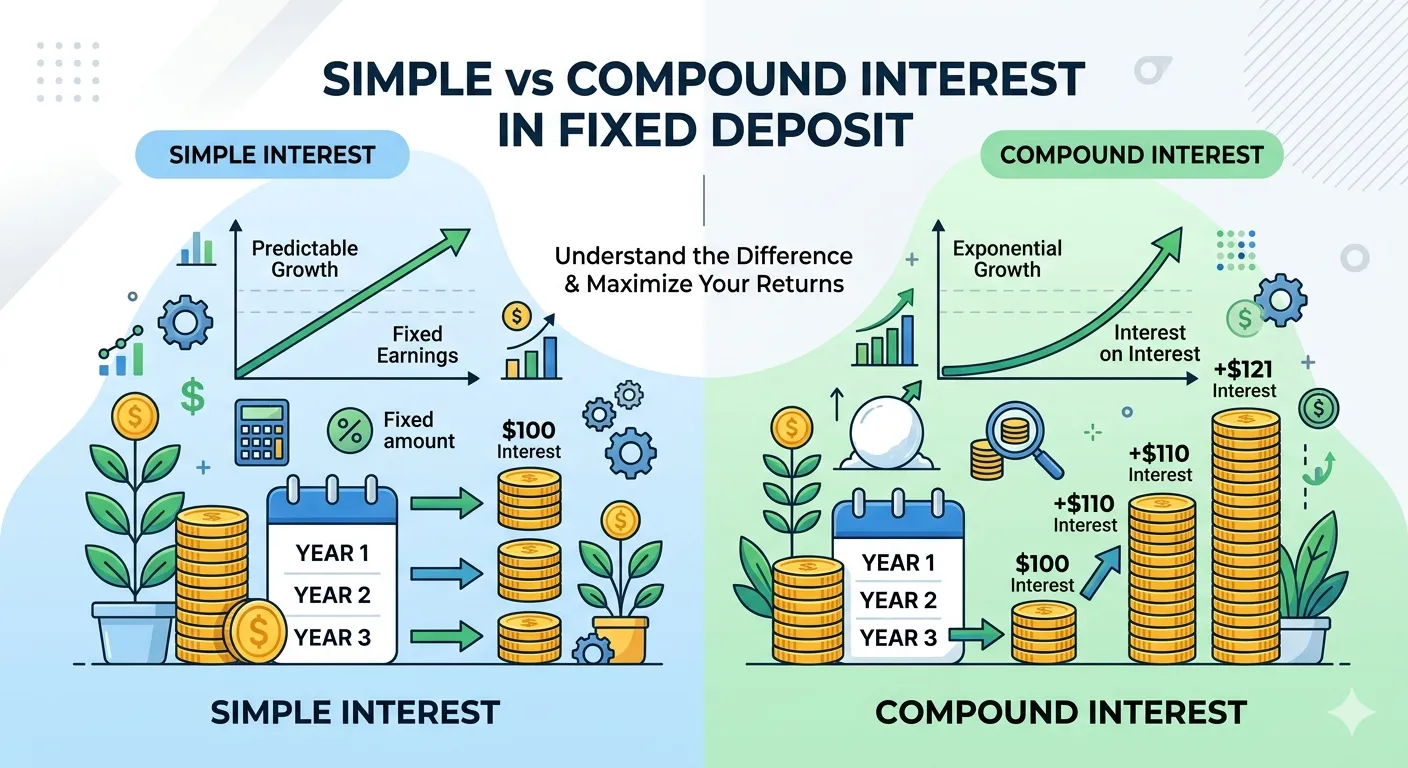

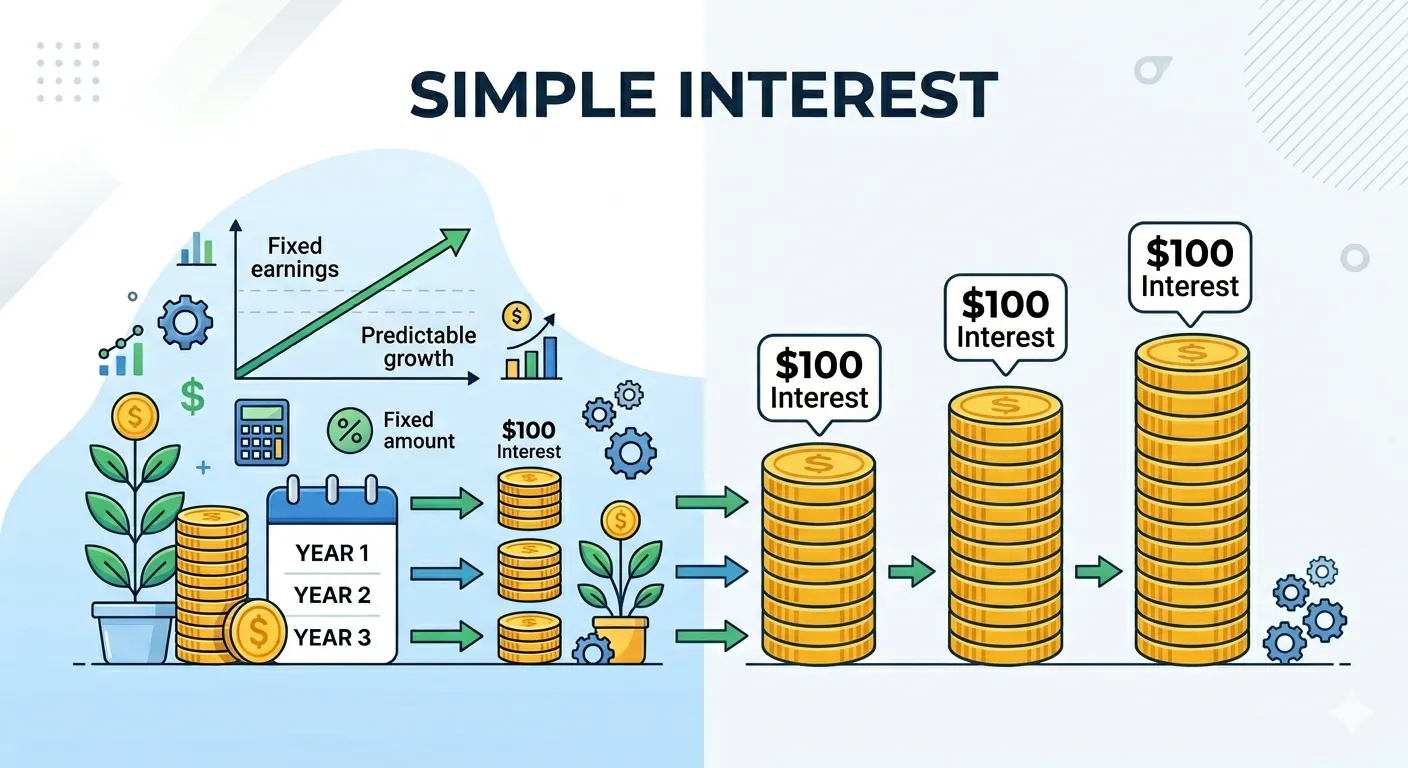

What Is Simple Interest?

Simple interest is calculated only on the original deposit amount (principal). The interest earned each year remains the same throughout the tenure.

Simple Interest (SI) = P × r × t

- P = Principal amount

- r = Annual interest rate (in decimal form)

- t = Time in years

In simple interest, the interest does not earn further interest. This makes it easy to calculate but usually less rewarding over longer durations.

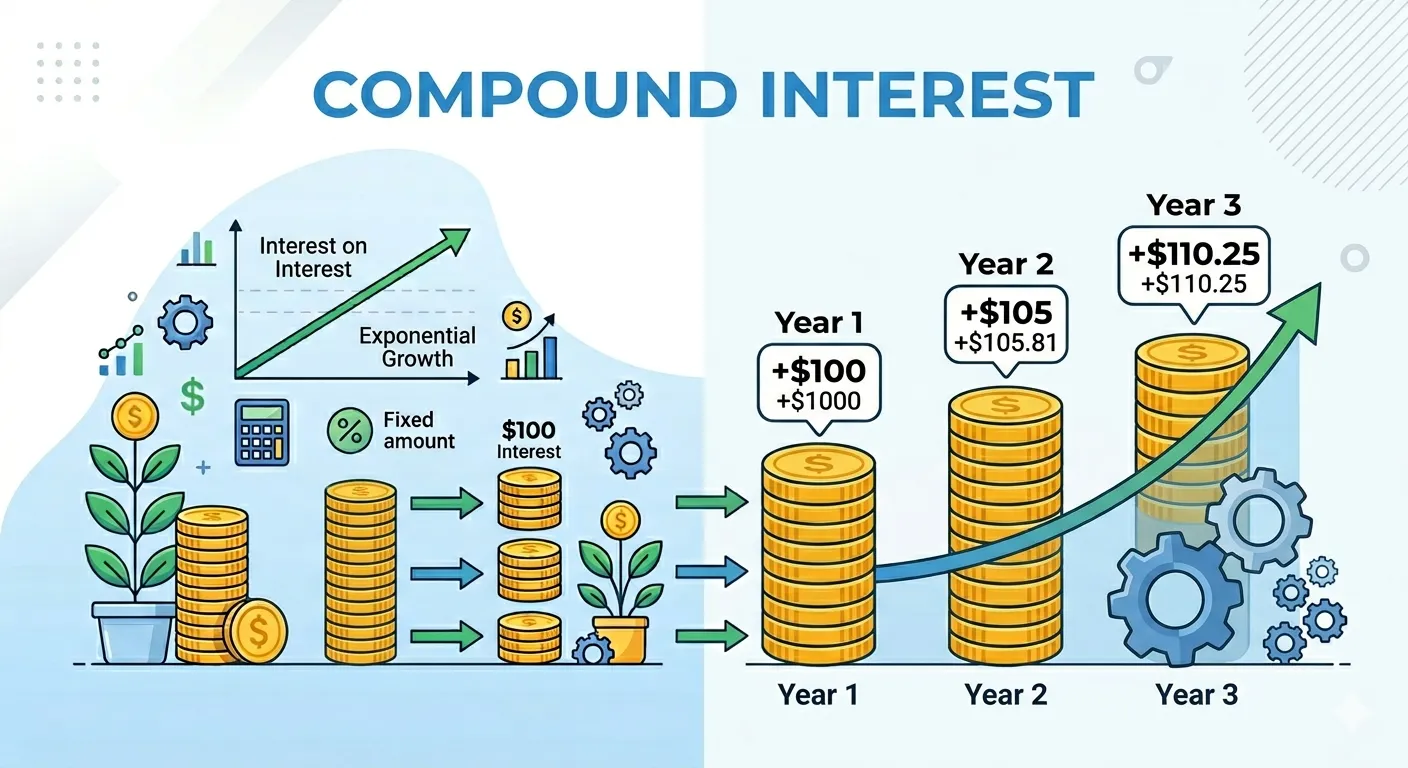

What Is Compound Interest?

Compound interest is calculated on both the principal and the accumulated interest. In other words, interest earns interest over time.

A = P × (1 + r/n)n×t

- A = Final maturity amount

- P = Principal amount

- r = Annual interest rate (in decimal form)

- n = Number of compounding periods per year

- t = Time in years

Most bank fixed deposits use compound interest, typically compounded quarterly. This is why FD returns are usually better than simple-interest products for the same rate and tenure. For bank-specific estimates, try the HDFC Bank FD Calculator and compare the output with our ICICI FD Calculator.

Simple vs Compound: Full Comparison

| Parameter | Simple Interest | Compound Interest |

|---|---|---|

| Interest calculated on | Principal only | Principal + accumulated interest |

| Growth pattern | Linear | Exponential over time |

| Returns for long tenure | Lower | Higher |

| Calculation complexity | Simple | Moderate |

| Common use in FDs | Rare | Very common |

| Best suited for | Short, straightforward plans | Wealth growth over medium/long tenure |

Formulas and Worked Examples

Let us compare both methods with the same FD details:

- Principal: $1,00,000

- Interest rate: 7% per annum

- Tenure: 3 years

Example 1: Simple Interest

SI = 1,00,000 × 0.07 × 3 = $21,000

Maturity Amount = $1,21,000

Example 2: Compound Interest (Quarterly)

A = 1,00,000 × (1 + 0.07/4)4×3

A = 1,00,000 × (1.0175)12 ≈ $1,23,043

Maturity Amount ≈ $1,23,043

Longer Tenure Impact (5 years, same rate)

| Method | Maturity Amount | Total Interest Earned |

|---|---|---|

| Simple Interest | $1,35,000 | $35,000 |

| Compound Interest (Quarterly) | ≈ $1,41,404 | ≈ $41,404 |

Which Is Better for Fixed Deposits?

For most investors, compound interest is better because it gives higher maturity value, especially for longer tenures. However, the right choice also depends on your cash-flow needs.

Simple Interest may suit you if:

- You need predictable fixed interest payout logic

- Your tenure is short and return difference is minimal

- You prefer very easy manual calculation

Compound Interest is usually better if:

- You are investing for 1 year or more

- You want maximum FD maturity value

- You can keep funds invested without frequent withdrawals

Frequently Asked Questions

Do all fixed deposits use compound interest?

Most bank FDs use compound interest (often quarterly), but specific payout variants may differ by bank.

Why does compounding frequency matter?

More frequent compounding generally increases returns because interest is added to principal more often.

Is simple interest ever better than compound interest?

Simple interest can be easier to track, but for the same rate and tenure, compound interest usually gives higher returns.

How can I quickly compare both methods?

Use the formulas above or an online tool. Our FD Calculator helps estimate maturity instantly.